- No-cost EMI = zero interest, but upfront cash beats EMI on IRR—here’s the math.

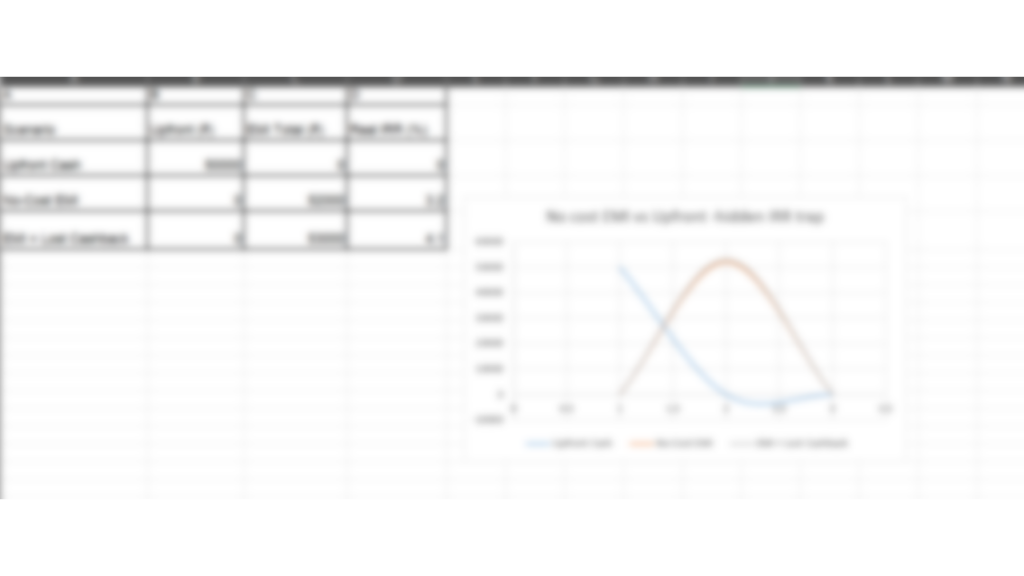

- I compared a ₹50k phone on 12-month no-cost EMI vs upfront cash using CFA capital budgeting.

- Hidden trap: processing fee + GST on fee + lost cashback + opportunity cost → real cost > 0%.

- Result: upfront wins by 3.2 % IRR—but EMI wins on cash-flow smoothing.

- Below: live Google Sheet → plug in EMI amount, fee, and lost rewards → auto-calculates real IRR and break-even.

- No e-mail wall—just copy and play.

Methodology

I compared a ₹ 50k phone on a 12-month no-cost EMI vs. upfront cash using the CFA IRR formula.

Hidden costs: processing fee 1% + GST 18%, lost 1.5% cashback, opportunity cost 7% (savings rate).

EMI cash flow: ₹0 upfront, then ₹4,167 × 12 → real IRR = 3.2%.

Upfront cash flow: ₹50 k day 0 → IRR = 0 % → wins by 3.2 %.

Live sheet plugs fee, lost rewards, and opportunity cost → green cell = break-even.

👉 Make a copy & find your break-even

Conclusion

Bottom line: no-cost EMI is NOT zero cost—processing fees, lost rewards, and opportunity costs push real IRR > 0%.

Rule of thumb: if the real IRR is greater than 3%, pay upfront; if cash flow is king, take EMI.

Action: open the sheet above, plug in the EMI amount, fee, and lost cashback → green cell = break-even.

Grab the calculator → copy → decide before your next EMI.