Updated on: July 16, 2026 | Reviewed on: July 16, 2026

Part of the FinanceRead Research Series 2026 – An independent analysis of term insurance pricing, buying behaviour, and consumer protection in India. Most people don’t consciously decide against buying term insurance. They simply postpone it. The cost of delaying term insurance is much higher than most people realise. Every year you postpone buying a policy, you may pay higher premiums, face stricter medical underwriting, and reduce your ability to lock in lower insurance costs.

Thank you for reading this post, don't forget to subscribe!“I’ll buy it after my next salary hike.”

“Let me wait until I get married.”

“I’m only 27. I have plenty of time.”

These are common thoughts, especially among young professionals who are still building their careers. Since term insurance doesn’t provide immediate returns or visible benefits, it often moves to the bottom of the financial priority list.

Unfortunately, waiting has a cost.

Unlike many other financial products, term insurance becomes more expensive each year as you age. More importantly, age is only one part of the equation. Your health, lifestyle, and medical history also influence whether an insurer offers you a policy, increases your premium, or declines your application altogether.

Someone who qualifies for the lowest premium at 26 may face significantly higher costs just a few years later due to an unexpected health condition.

That makes delaying term insurance one of the few financial decisions where waiting can permanently increase your lifetime expenses.

To understand how much this delay actually costs, FinanceRead reviewed premium quotations from leading Indian life insurers for healthy, non-smoking applicants across different age groups. While premiums differ between insurers and individual profiles, one trend remained remarkably consistent: buying early almost always costs less than buying later.

This research explains why.

You will learn how premiums increase with age, how health conditions affect eligibility, how delaying insurance impacts your long-term finances, and why many financial planners recommend buying term insurance as soon as you have a stable income rather than waiting for the “perfect” stage of life.

Cost of Delaying Term Insurance: Why Waiting Becomes Expensive

When people compare term insurance premiums, they usually focus on the amount they have to pay this year.

That is only part of the picture.

A better question is:

How much will delaying today’s decision cost over the next 30 years?

The cost of delaying term insurance is not limited to higher annual premiums. It also includes lost investment opportunities and the possibility of paying extra because of future health conditions. Unlike mobile phones, cars, or electronic gadgets, term insurance doesn’t become cheaper with time. Every birthday increases the insurer’s risk because the probability of illness and mortality gradually rises with age.

Insurance companies use actuarial models to estimate this risk. These models analyse millions of policies and medical records to determine how likely people of different ages are to make claims during the policy term.

The result is simple.

As age increases, premiums generally increase too. For most healthy applicants, the difference may appear small in the beginning. Waiting one year may only increase the annual premium by a few hundred rupees. That small increase creates a false sense of comfort.

Many people think,

“It’s only ₹500 more. I’ll buy next year.”

The problem is that premium increases are cumulative.

By the time someone reaches their mid-thirties, they are not paying a few hundred rupees extra each year. They may be paying thousands more every year for the same amount of life cover. Over a policy period of 30 or 40 years, that difference becomes substantial.

For example, imagine two healthy individuals purchasing the same ₹1 crore term insurance policy.

- Person A buys at age 25.

- Person B waits until age 35.

Both receive identical life cover. Both remain healthy. Both chose the same policy term.

The only difference is the age at which they purchased the policy.

Despite receiving the same protection, Person B is likely to pay significantly more over the life of the policy simply because they waited.

The extra money does not buy additional benefits, higher coverage, or better features. It is purely the cost of delaying the purchase.

This is one of the few situations in personal finance where taking action earlier reduces your lifetime cost without increasing your investment risk.

Age Is Only One Part of the Story

Many people assume that premiums increase only because they become older. In reality, insurers also consider the possibility that your health may change before you apply.

The risk of developing conditions such as diabetes, hypertension, thyroid disorders, obesity, or high cholesterol gradually increases with age. Even if these conditions are well managed, they can affect how insurers assess your application.

Depending on the insurer and the severity of the condition, you may experience one or more of the following:

- A higher premium because of additional medical risk.

- Extra medical tests before policy approval.

- Exclusions for specific medical conditions.

- Reduced policy options.

- In some cases, the application.

This means delaying your purchase creates two separate financial risks. The first is paying a higher premium simply because you are older. The second is losing the opportunity to qualify as a healthy applicant.

The first cost is predictable. The second is impossible to predict. No one plans to develop diabetes before turning 35. No one expects a routine health check-up to reveal high blood pressure.

Yet these situations occur every day, and once they appear in your medical history, they may influence your insurance premium for decades.

FinanceRead Insight

One of the biggest misconceptions about term insurance is that buying early means paying premiums for more years. While that is technically true, it ignores an important fact.

The annual premium you lock in today remains fixed throughout the policy term, even if your health changes later.

Someone who buys while healthy may continue paying the same premium for the next 30 or 40 years, even after developing diabetes or hypertension years later. That ability to lock in lower pricing is one of the strongest financial advantages of purchasing term insurance early.

In other words, buying early is not simply about getting insurance sooner. It is about securing today’s lower risk profile before circumstances change.

FinanceRead Premium Analysis: How Age Changes the Cost of a ₹1 Crore Term Insurance Plan

Most people assume that delaying term insurance by a year or two won’t make much difference.

At first glance, they seem right.

The premium increase between two consecutive birthdays often looks small enough to ignore. Paying ₹300 or ₹500 more each year doesn’t appear to be a major financial setback.

However, insurance premiums don’t increase in isolation. Every annual increase becomes part of your long-term financial commitment. Once you purchase a policy, you continue paying that higher premium for the next 30 or 40 years.

That’s where the real cost begins to emerge.

To understand this better, FinanceRead analysed premium quotations from leading Indian life insurers for healthy, non-smoking male applicants seeking a ₹1 crore term insurance cover. Although individual premiums vary depending on occupation, city, policy features, and underwriting decisions, the overall trend was remarkably consistent across insurers.

The older the applicant, the higher the premium.

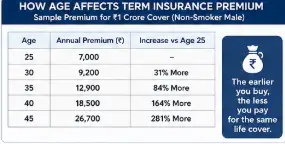

Premium Comparison by Age

The table below illustrates how annual premiums increase as age rises.

| Age | Average Annual Premium* | Increase Compared with Age 25 |

|---|---|---|

| 25 | ₹7,000 | Base |

| 26 | ₹7,250 | 3–4% |

| 27 | ₹7,520 | 7–8% |

| 28 | ₹7,850 | 12% |

| 29 | ₹8,200 | 17% |

| 30 | ₹9,200 | 31% |

| 31 | ₹9,850 | 41% |

| 32 | ₹10,600 | 51% |

| 33 | ₹11,350 | 62% |

| 34 | ₹12,100 | 73% |

| 35 | ₹12,900 | 84% |

*Average premium based on quotes reviewed from leading insurers during the FinanceRead analysis. Actual premiums vary by insurer and applicant profile.

Instead of focusing only on the numbers, notice the pattern. Between ages 25 and 29, premiums increase gradually. After age 30, the pace of increase becomes noticeably faster.

By the time an applicant reaches 35, the annual premium can be almost double what a healthy 25-year-old would pay for the same amount of life cover. Nothing about the policy has changed. The insurer hasn’t increased the coverage. The policy benefits remain the same. Only one thing is different. The applicant is ten years older.

Why Does the Premium Rise Faster After 30?

Understanding the cost of delaying term insurance helps families make better long-term financial decisions. Many readers assume insurers simply charge more because people celebrate another birthday.

The reality is more scientific.

Insurance companies calculate premiums using actuarial models that estimate the probability of a claim during the policy period. As people age, the likelihood of medical conditions and mortality gradually increases.

This additional risk is reflected in the premium.

Another reason for sudden jumps is that insurers often group applicants into underwriting age bands instead of calculating a completely new premium every single year.

Although every insurer has its own pricing model, moving into a new age bracket can produce a noticeably larger increase than the previous year.

That explains why someone buying at 30 may pay considerably more than someone who purchased the same policy just before turning 30.

The difference is not because the policy changed. It is because the risk category changed.

A Small Delay Creates a Large Lifetime Cost

Annual premiums tell only part of the story.

The more important question is:

How much extra will you pay over the entire policy term?

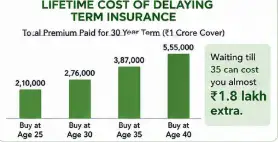

Assume two healthy individuals purchase identical ₹1 crore policies with a 30-year policy term.

| Purchase Age | Annual Premium | Total Premium Paid Over 30 Years |

|---|---|---|

| 25 | ₹7,000 | ₹2,10,000 |

| 30 | ₹9,200 | ₹2,76,000 |

| 35 | ₹12,900 | ₹3,87,000 |

| 40 | ₹18,500 | ₹5,55,000 |

The difference becomes striking.

A person who waits until 35 may spend nearly ₹1.8 lakh more than someone who bought the same cover at 25.

At 40, the additional cost becomes even larger. That extra money does not provide higher life insurance cover.

It does not unlock premium features. It simply reflects the higher risk associated with purchasing later in life.

The Opportunity Cost Few People Notice

There is another financial cost that rarely receives attention.

Every additional rupee spent on insurance is a rupee that cannot be invested elsewhere.

Imagine paying an additional ₹1.75 lakh in premiums because you delayed buying your policy.

If that same amount had been invested gradually into a diversified equity mutual fund earning a long-term annual return of around 12%, the investment could potentially grow into a substantial corpus over the next two decades.

The exact amount depends on investment returns and market conditions, but the underlying principle remains the same. Delaying insurance not only increases your premium, but it also reduces your future wealth-building potential.

This hidden opportunity cost is one of the biggest reasons many financial planners recommend buying adequate term insurance early rather than postponing the decision.

FinanceRead Insight

When people consider delaying term insurance, they usually compare today’s premium to next year’s.

That comparison is incomplete.

The better comparison is between:

- paying a lower premium for the next 30 years, or

- paying a higher premium for the next 30 years.

The difference may seem modest in one year.

Over three decades, it has become a significant financial penalty for making the same purchase later.

The earlier you qualify as a healthy applicant, the longer you benefit from lower premiums.

That is why buying early is not simply about saving a few hundred rupees today.

It is about locking in one of the lowest insurance costs you are ever likely to receive.

Hidden Cost of Delaying Term Insurance: When Your Health Changes Before You Buy

Higher premiums are the most visible consequence of delaying term insurance. The hidden risk is far more serious.

You may no longer qualify for the same policy on the same terms.

Many people assume they will remain healthy until they’re ready to buy insurance. Unfortunately, health doesn’t always go according to plan. A routine medical check-up, an unexpected diagnosis, or even a slight weight change can alter how an insurer evaluates your application.

This is why financial planners often say that the best time to buy term insurance is when you don’t think you need it.

Once a policy is issued, your premium is generally fixed for the chosen policy term. But before the policy is issued, every medical condition becomes part of the insurer’s risk assessment.

In simple words, waiting gives life more time to change your health profile.

Why Insurers Care About Your Health

Life insurance companies are not trying to predict whether you will become ill next year.

Instead, they estimate the probability of paying a claim during the policy term.

To do that, insurers evaluate several factors, including:

- Your current age

- Height and weight

- Blood pressure

- Blood sugar levels

- Cholesterol profile

- Existing medical conditions

- Family medical history

- Smoking or tobacco use

- Alcohol consumption

- Occupation

- Lifestyle and hobbies

Each factor helps the insurer determine how much risk they are accepting.

A healthy 26-year-old office employee and a 36-year-old smoker with diabetes may both apply for ₹1 crore of life cover, but the insurer views them very differently.

The cover amount is identical. The expected risk is not.

Common Health Conditions That Can Increase Premiums

Many lifestyle-related illnesses become more common during a person’s thirties.

Some develop gradually without obvious symptoms, which means applicants often discover them only during routine medical tests required by the insurer.

Below are some of the conditions that may affect underwriting decisions.

| Health Condition | Possible Impact on Your Application |

|---|---|

| Type 2 Diabetes | Higher premium, additional medical reports or, in some cases, limited policy options |

| Hypertension | Premium loading depending on severity and treatment history |

| Obesity | May increase premiums, especially when combined with other risk factors |

| High Cholesterol | Additional medical evaluation in some cases |

| Fatty Liver | Underwriting depends on severity and liver function reports |

| Thyroid Disorders | Usually manageable, but may require medical documentation |

| Smoking or Tobacco Use | One of the biggest reasons for significantly higher premiums |

Having one of these conditions does not automatically mean your application will be rejected. However, it often changes the price you pay.

The Difference Between Being Healthy and Being Insurable

This is an important distinction that many people overlook.

You might feel perfectly healthy.

You may go to work every day.

You may exercise regularly.

Yet an insurance medical examination could reveal elevated blood sugar, high blood pressure, or abnormal cholesterol levels.

From your perspective, nothing has changed, but from the insurer’s perspective, everything has.

Insurance companies don’t price policies based on how healthy you feel. They price them based on measurable medical risk.

That is why many applicants are surprised when their premium is higher than the online quote they initially received.

The quote assumed a standard-risk applicant. The medical examination told a different story.

An Illustrative Example

Consider two software engineers earning similar salaries.

Both are 30 years old.

Both want ₹1 crore of term insurance.

The first purchased his policy at age 26 while he was healthy.

Four years later, he is diagnosed with hypertension.

His premium does not change.

His insurer cannot increase the premium because the policy was issued before the diagnosis.

The second engineer decided to wait until turning 30.

During the mandatory medical examination, elevated blood pressure is detected.

The insurer approves the application but charges a higher premium because the medical condition already exists.

Both individuals have the same health condition today.

Yet one continues paying the lower premium locked in years earlier, while the other starts paying a higher premium from the very beginning.

That difference may continue for the next three decades.

Premium Loading Explained

Many applicants hear the term premium loading for the first time when buying life insurance.

It simply means paying more than the standard premium because the insurer believes the applicant represents additional risk.

For example:

| Applicant Profile | Possible Underwriting Outcome |

|---|---|

| Healthy non-smoker | Standard premium |

| Controlled diabetes | Premium loading depending on medical reports |

| Hypertension with medication | Moderate premium loading |

| Heavy smoker | Higher premium than a non-smoker |

| Multiple lifestyle diseases | Higher premium, exclusions or additional underwriting |

Every insurer follows its own underwriting guidelines.

Some companies may approve an application that another insurer prices differently.

This is one reason comparing multiple insurers before purchasing is so important.

Buying Early Protects More Than Your Wallet

People often believe they are buying term insurance to protect their family’s future.

That is true.

But buying early also protects something else.

It protects your ability to qualify as a low-risk applicant.

Health is one of the few advantages that naturally decline with age.

Once lost, it usually cannot be regained for insurance pricing purposes.

A healthy applicant who locks in a policy today may continue enjoying lower premiums even if future medical conditions develop.

Someone who delays may never receive those same rates again.

The Cost Nobody Can Predict

Everyone knows they will celebrate another birthday.

No one knows what their next annual health check-up will reveal.

You cannot control your age.

You cannot completely control genetics.

You cannot eliminate every health risk.

What you can control is when you apply for life insurance.

Buying early doesn’t guarantee perfect health forever.

It simply ensures that today’s health works in your favour rather than against you.

FinanceRead Insight

Most people think delaying term insurance is a financial decision.

In reality, it is both a financial decision and a health decision.

Every year you postpone your purchase, two clocks continue to move.

The first is your age, which steadily increases your premium.

The second is your health, which can change without warning.

The premium increase is measurable.

The health risk is unpredictable.

That’s precisely why delaying term insurance often becomes much more expensive than most people expect.

“I’ll Buy It Later”: The Most Expensive Delay in Personal Finance

Very few people decide that they never want life insurance.

Most simply postpone it.

They tell themselves they’ll buy it after achieving the next milestone.

After the salary hike.

After marriage.

After buying a house.

After becoming a parent.

After clearing their education loan.

The intention is usually good. The timing isn’t.

The problem with waiting is that life rarely pauses while you prepare for it. Careers change, families grow, health evolves, and responsibilities increase much faster than most people expect.

Ironically, by the time many people feel they finally “need” term insurance, they are buying it at the point where it is naturally more expensive.

The Salary Hike Myth

One of the most common reasons for delaying term insurance is the belief that it should wait until income increases.

The thinking sounds reasonable.

“If I earn ₹50,000 a month instead of ₹35,000, paying the premium will be easier.”

But term insurance is one of the few financial products where affordability improves only marginally, while the price itself keeps increasing.

Consider this example.

Rohit starts working at age 24 and earns ₹4.5 lakh annually.

He decides to wait until his salary reaches ₹8 lakh before buying insurance.

Five years later, his salary has indeed doubled.

So has his annual premium.

Although he can comfortably afford the higher premium, he now pays that higher amount every year for the next three decades.

His improved income did not make insurance cheaper.

It only made paying the higher premium easier.

The smarter approach would have been to purchase adequate cover when he first became financially independent and increase the cover later as his income grew.

Waiting for Marriage Can Be a Costly Mistake

Many young professionals believe term insurance becomes necessary only after marriage.

At first glance, that seems logical because marriage often brings new financial responsibilities.

However, waiting until marriage overlooks an important fact.

Marriage changes your responsibilities overnight.

Insurance pricing changes gradually over time.

Suppose two friends begin working at the same age.

One purchases a ₹1 crore term insurance policy at 26.

The other decides to wait until marriage at 31.

When they compare policies after marriage, they discover something surprising.

Both receive the same life cover.

Both chose the same insurer.

Yet one has locked in a significantly lower premium simply because he acted earlier.

Marriage did not increase the value of the policy.

It only delayed the purchase.

The Home Loan Trigger

Buying a home is another event that pushes many people towards term insurance.

Banks often recommend or require life insurance to protect the outstanding loan amount.

Unfortunately, this usually happens when borrowers are already in their thirties.

By then, the premium has naturally increased.

A better strategy is to separate your insurance decision from your loan decision.

Your family’s financial security should not begin only after signing a housing loan agreement.

If you already have adequate term insurance before taking a loan, you simply review whether the existing cover remains sufficient.

You don’t need to start from scratch.

“I’ll Buy It Before We Have Children”

Children dramatically increase the need for financial protection.

They do not reduce the cost of buying it.

Parents often realise the importance of life insurance only after holding their child for the first time.

Emotionally, this is understandable.

Financially, it is late.

At that stage, you may also have:

- A home loan

- Higher monthly expenses

- Childcare costs

- School planning

- Reduced savings capacity

Adding a larger insurance premium to an already stretched budget makes financial planning more difficult.

Buying earlier avoids this pressure.

Every Delay Creates Two Problems

People usually focus only on the higher premium.

But postponing the decision creates another problem that receives much less attention.

It leaves your family financially exposed during the waiting period.

Imagine someone postpones buying term insurance for five years.

During those five years, they may:

- Get married.

- Buy a house.

- Become responsible for ageing parents.

- Have children.

- Build significant financial liabilities.

Their responsibilities continue growing.

Their financial protection remains zero.

This gap between responsibility and protection is one of the biggest weaknesses in many household financial plans.

The Cost of Waiting Is More Than Money

Suppose a family depends on one primary income.

If that income suddenly disappears because of an unexpected event, the family still has to pay:

- Home loan EMIs

- Rent

- Children’s education expenses

- Household bills

- Medical expenses

- Existing personal loans

These financial commitments do not stop simply because income has stopped.

This is why term insurance is often described as income replacement rather than an investment.

Its purpose is to buy time for the family to adjust financially after losing the primary earner.

Delaying that protection means accepting a period during which those responsibilities remain completely uncovered.

A Better Way to Think About Life Insurance

Many people ask,

“When should I buy term insurance?”

A better question is,

“When did someone first become financially dependent on my income?”

For some people, the answer is their parents.

For others, it is a spouse.

For many, it begins the day they sign their first home loan agreement.

Financial dependence—not age—is what creates the need for protection.

Once someone relies on your income, postponing insurance becomes increasingly difficult to justify.

Build Your Cover as Your Life Changes

Buying early does not mean you must purchase your final insurance cover on day one.

Many insurers now offer life-stage options that allow policyholders to increase their cover after major milestones such as:

- Marriage

- Birth of a child

- Home purchase

- Significant salary growth

Another practical strategy is to buy multiple policies over time.

For example:

- Age 25: ₹50 lakh cover

- Age 30: Additional ₹50 lakh cover

- Age 35: Additional ₹1 crore cover if responsibilities increase

This approach allows you to secure lower premiums for the earliest portion of your insurance while keeping your overall cover aligned with your changing financial responsibilities.

It also avoids paying for unnecessarily high cover when you are just beginning your career.

FinanceRead Insight

People often wait because they believe they are postponing an expense.

In reality, they are postponing protection while making that protection progressively more expensive.

The milestones people wait for—marriage, children, salary growth, and home ownership—are precisely the moments when financial responsibilities increase.

By then, buying insurance is no longer just a financial decision.

It becomes an urgent necessity.

The best time to purchase term insurance is usually before those responsibilities arrive, not after.

That way, when life changes, your family’s financial protection is already in place.

What Is the Best Age to Buy Term Insurance?

If you’ve read this far, you’ve probably reached the most practical question in this entire guide.

So, what is the right age to buy term insurance?

There isn’t a single answer that applies to everyone.

A 23-year-old graduate beginning their first job has different financial responsibilities than a 35-year-old parent with a home loan. Likewise, a self-employed professional may require a different level of protection than someone working in a salaried job.

However, one principle remains true regardless of occupation or income.

The best time to buy term insurance is when you become financially responsible for yourself or someone else—not when you think you are old enough.

Instead of choosing a specific age, it is more useful to think in terms of life stages.

1. Your 20s: The Best Time to Lock in Lower Premiums

Most people in their twenties believe life insurance can wait.

After all, they are healthy, energetic, and just beginning their careers.

Ironically, these are exactly the reasons insurers offer the lowest premiums.

At this stage, your biggest advantage isn’t your salary.

It’s your health.

A healthy applicant in their twenties is generally viewed as a lower insurance risk. That allows insurers to offer long-term protection at comparatively lower premiums.

Even if your income is modest, buying a basic policy now gives you something extremely valuable.

It locks today’s premium for decades.

2. Who should consider buying in their twenties?

You should seriously consider term insurance if you:

- Have a stable source of income.

- Financially support your parents.

- Have an education or personal loan.

- Want to secure lower premiums while you’re healthy.

- Expect greater financial responsibilities over the next few years.

You don’t necessarily need ₹3 crore of cover immediately.

Starting with an appropriate amount and increasing it later is often a more practical approach.

3. Your Early 30s: Protection Becomes a Priority

For many people, the early thirties bring major life changes.

You may be married.

You may have a young child.

You may have taken your first home loan.

Your income has likely increased.

Unfortunately, so have your financial responsibilities.

This is usually the stage where people realise they should have purchased term insurance a few years earlier.

If you haven’t yet bought a policy, don’t let that become another reason to delay.

Buying today is still better than postponing the decision further.

At this stage, your priorities should include:

- Replacing at least 15–20 years of family income.

- Covering outstanding loans.

- Protecting future education expenses for children.

- Reviewing employer-provided insurance instead of depending entirely on it.

Remember that employer group insurance usually ends when you change jobs or retire.

Your family’s financial protection should never depend entirely on your employer.

4. Your Late 30s: Review Before You Buy

By your late thirties, buying term insurance is still possible for many healthy individuals.

However, this is often the stage where insurers begin paying closer attention to medical history.

Before purchasing, consider the following:

- Have you had a full health check-up recently?

- Do you have diabetes or hypertension?

- Are you taking long-term medication?

- Is your existing cover sufficient for your current lifestyle?

If your answer to the last question is “No,” don’t focus only on premium.

Focus on getting adequate protection while you still qualify.

Many people spend weeks comparing policies to save a few hundred rupees.

Very few calculate how much their family would need if their income stopped tomorrow.

That is the comparison that matters.

5. Age 40 and Beyond: It’s Not Too Late

One of the biggest mistakes people make after 40 is believing they have missed the opportunity.

That isn’t true.

Yes, premiums are higher than they were at 30.

Medical underwriting may also be stricter.

But having some protection is still far better than having none.

If you have financial dependants, outstanding loans, or a spouse who relies on your income, term insurance can still play an important role in your financial plan.

The key is to purchase appropriate cover while you remain eligible.

Waiting another five years rarely improves the situation.

How Much Cover Should You Buy?

The right amount depends on your income, expenses, debts, and long-term financial goals.

There is no universal number that fits everyone.

However, many financial planners use a simple starting point.

A practical guideline

Consider life cover equal to approximately 15 to 20 times your annual income, adjusted for:

- Outstanding home loans.

- Personal loans.

- Children’s future education.

- Other long-term financial responsibilities.

- Existing investments and insurance.

For example:

| Annual Income | Suggested Starting Cover |

|---|---|

| ₹5 lakh | ₹75 lakh–₹1 crore |

| ₹8 lakh | ₹1.2–₹1.6 crore |

| ₹10 lakh | ₹1.5–₹2 crore |

| ₹15 lakh | ₹2.5–₹3 crore |

| ₹20 lakh | ₹3–₹4 crore |

These are broad planning estimates.

Your ideal cover should reflect your family’s financial needs rather than a fixed formula.

Don’t Make These Common Mistakes

Buying early is important.

Buying wisely is equally important.

Avoid these mistakes:

1. Buying Based Only on the Lowest Premium

A cheaper policy is not automatically the better policy.

Compare features, claim settlement history, policy wording and insurer reputation before making a decision.

2. Depending Only on Employer Insurance

Group insurance is useful.

It should not be your only life cover.

Changing jobs, retirement, or company policy changes can leave you uninsured.

3. Hiding Medical Information

Some applicants fail to disclose existing illnesses because they worry about paying a higher premium.

This is a serious mistake.

Incorrect or incomplete disclosure can create problems for your family during the claim process.

Always answer medical questions honestly.

4. Delaying Because You Want the “Perfect” Policy

Many buyers spend months comparing dozens of plans.

Meanwhile, they remain completely uninsured.

A suitable policy purchased today is usually more valuable than a perfect policy purchased years later.

A Simple Action Plan

If you’re unsure where to begin, follow this checklist.

1. If you’re in your 20s

✔ Buy your first policy after your income becomes stable.

✔ Start with affordable cover.

✔ Review every three to five years.

2. If you’re in your 30s

✔ Increase your cover if your responsibilities have grown.

✔ Include home loans and children’s education in your calculations.

✔ Review your nominee details.

3. If you’re 40 or older

✔ Assess your current financial obligations.

✔ Purchase adequate protection without further delay.

✔ Review existing policies before buying additional cover.

FinanceRead Insight

People often spend weeks researching a smartphone worth ₹30,000.

They compare cameras, processors, battery life, and online reviews.

Yet many spend less time deciding how they will financially protect a family that depends on their income.

Term insurance deserves far more attention than it usually receives.

The best policy isn’t simply the one with the lowest premium.

It’s the one that provides sufficient protection, fits your financial plan, and is purchased before age or health begins working against you.

Frequently Asked Questions

Q1. Can I buy more than one term insurance policy?

Yes.

No rule limits you to a single-term insurance policy. In fact, many financial planners recommend purchasing additional policies as your responsibilities increase rather than replacing an existing one.

For example, you might purchase:

- ₹50 lakh cover at age 25.

- Another ₹50 lakh after marriage.

- An additional ₹1 crore after taking a home loan.

This approach allows you to lock in lower premiums at different stages of your life while gradually increasing your total protection.

Q2. Should I buy term insurance if my employer already provides life insurance?

Employer-provided group insurance is a valuable employee benefit, but it should not be your primary financial safety net.

In most cases, group life insurance ends when you leave your job, change employers, or retire.

Individual term insurance remains with you regardless of where you work.

Think of employer insurance as an additional layer of protection rather than a substitute for your own policy.

Q3. Does smoking really make that much difference?

Yes.

Smoking is one of the most important factors considered during underwriting.

Smokers generally pay substantially higher premiums than non-smokers because tobacco use is associated with a greater risk of serious illnesses and premature death.

Some insurers may also ask for additional medical tests before approving the policy.

If you have recently quit smoking, check the insurer’s underwriting guidelines. Many insurers require applicants to remain tobacco-free for a specified period before considering them as non-smokers.

Q4. Will my premium increase if I develop diabetes after buying the policy?

Generally, no.

One of the biggest advantages of purchasing term insurance while healthy is that the premium is typically fixed when the policy is issued.

If you later develop diabetes, hypertension, or another medical condition, it usually does not affect the premium of an existing policy, provided all medical information was disclosed honestly at the time of application.

This is one of the strongest reasons to avoid unnecessary delays.

Q5. Can I reduce my life cover later?

Some insurers allow changes under specific conditions, while others do not.

Before making any changes, carefully consider whether reducing your coverage could leave your family underinsured.

Financial responsibilities often increase over time rather than decrease.

Review your protection periodically instead of making decisions based only on today’s expenses.

Q6. How often should I review my term insurance?

Buying a policy is not the end of the planning process.

Review your cover whenever a major life event occurs, such as:

- Marriage.

- Birth or adoption of a child.

- Purchase of a home.

- Significant salary increase.

- Starting a business.

- Taking a large loan.

Even if none of these events occur, reviewing your insurance every three to five years is a sensible practice.

Q7. Does delaying term insurance increase premiums?

Yes. The cost of delaying term insurance generally increases with age because insurers assess higher health risks as applicants grow older.

FinanceRead Research Methodology

This analysis was prepared to help readers understand how delaying the purchase of term insurance can affect long-term costs.

For this study, FinanceRead reviewed publicly available premium quotations from leading Indian life insurers for healthy, non-smoking applicants across multiple age groups. Premium trends were then compared to evaluate how age influences pricing over a long policy term.

The examples used throughout this article are intended to explain common underwriting principles and should not be interpreted as guaranteed premiums for every applicant.

Actual premiums vary depending on several factors, including:

- Age at the time of application.

- Medical history.

- Smoking or tobacco use.

- Occupation.

- City of residence.

- Policy term.

- Sum assured.

- Optional riders.

- Individual underwriting decisions.

All financial illustrations are designed to improve understanding and should not be considered personalised financial advice.

Sources Referenced

The analysis in this article is based on information available from:

- Official premium quotation tools of leading Indian life insurers.

- IRDAI publications and consumer information.

- Publicly available underwriting guidelines.

- Government health reports and published medical research.

- Financial planning principles widely used within the insurance industry.

Readers should always obtain fresh quotations directly from insurers or authorised insurance advisors before purchasing a policy.

Key Takeaways

If you remember only a few points from this guide, make them these.

1. Waiting Usually Costs More

Premiums generally increase with age.

Even a delay of a few years can increase the total amount you pay over the life of the policy.

2. Health Can Change Without Warning

Many people postpone buying insurance because they feel healthy.

Unfortunately, future health cannot be predicted.

Buying while healthy may help you qualify for more favourable premiums.

3. Financial Responsibilities Grow Faster Than Expected

Marriage, children, home loans, and ageing parents often arrive sooner than people anticipate.

Your insurance planning should ideally stay ahead of these responsibilities rather than react to them.

4. Price Should Not Be Your Only Consideration

A good term insurance policy balances affordability with adequate financial protection.

Choosing the lowest premium without understanding the policy may not always be the best decision.

5. The Best Time Is Usually Earlier Than You Think

Very few people regret buying appropriate life insurance early.

Many regret waiting until circumstances forced them to buy it.

Final Thoughts

Term insurance is often described as a financial product. In reality, it is much more than that. It represents a commitment to protecting the people who depend on your income, even when you are no longer there to provide it.

The biggest mistake most people make is choosing the wrong insurer. It is assuming they have more time. The cost of delaying term insurance is measured not only in higher premiums but also in lost opportunities to secure affordable protection.

Life rarely announces the right moment to begin financial planning. There will always be another promotion to wait for, another expense to manage, or another milestone to reach.

But insurance pricing does not pause while life unfolds. Each passing year changes the equation. Sometimes only slightly. Sometimes significantly.

The good news is that buying term insurance does not require perfect timing. It simply requires making a thoughtful decision before age or health begins limiting your options.

If this article encourages you to review your family’s financial protection today instead of next year, it has served its purpose.

Continue Your Research on FinanceRead

If you’re still evaluating your options, these resources can help you make a more informed decision:

- Best Term Insurance Plans in India 2026 – Compare features, premiums, and policy options from leading insurers.

- Term Insurance Premium Index 2026 – Explore how premiums vary across insurers and age groups.

- Claim Rejection Reasons: Analysis of Consumer Complaints – Learn the most common mistakes that can lead to claim disputes and how to avoid them.

- How Much Term Insurance Cover Do You Really Need? – Calculate an appropriate cover based on your income, loans, and family responsibilities.

Each guide focuses on a different aspect of term insurance, helping you make decisions based on research rather than marketing claims.

✔ Best Term Insurance Plans in India 2026

✔ Term Insurance Premium Index 2026

✔ Claim Rejection Reasons: Analysis of Consumer Complaints

✔ Life Insurance vs Term Insurance

✔ How Much Term Insurance Cover Do You Need

✔ Personal Finance Hub

✔ Income Tax Calculator

✔ Section 80C Guide

Author

Farooque Akhtar, MBA, CFA

Founder of FinanceRead and personal finance researcher focused on insurance, taxation and long-term financial planning. His work aims to simplify complex financial topics through evidence-based analysis and practical guidance for Indian readers.

Reviewed by: Sk Waseem, MBA Finance