- No-cost EMI = zero interest, but upfront cash beats EMI on IRR—here’s the math.

- I compared a ₹50k phone on 12-month no-cost EMI vs upfront cash using CFA capital budgeting.

- Hidden trap: processing fee + GST on fee + lost cashback + opportunity cost → real cost > 0%.

- Result: upfront wins by 3.2 % IRR—but EMI wins on cash-flow smoothing.

- Below: live Google Sheet → plug in EMI amount, fee, and lost rewards → auto-calculates real IRR and break-even.

- No e-mail wall—just copy and play.

This no cost emi vs upfront hidden IRR trap explains why zero-interest EMI schemes are often misleading for Indian buyers.

Thank you for reading this post, don't forget to subscribe!Why No Cost EMI Looks Cheap but Isn’t

Because they guarantee no interest payments, no cost EMI plans frequently seem appealing. The product price discount that you unknowingly forfeit, however, conceals the true cost. The opportunity cost is the only way to see the hidden IRR trap while deciding between an upfront payment and a no-cost EMI.

By eliminating the upfront discount given to cash buyers, banks are able to recoup interest. When this difference is translated into an annualized return, the effective interest rate is frequently significantly larger than that of standard EMIs. Many customers overlook this computation and believe that no-cost EMI is free.

No Cost EMI vs Upfront Hidden IRR Trap Explained

Because no interest is shown, no cost EMI frequently looks less expensive, but the true cost is concealed in the discount you forfeit by not making an advance payment. Only when the lost discount is turned into an annualized return via IRR computation does this no cost emi vs. upfront concealed IRR trap become evident.

How the Hidden IRR Trap Impacts Your Money

Buyers who could otherwise invest the upfront sum are primarily impacted by the hidden IRR trap. In certain situations, the implied IRR can surpass 20 percent per year when the forgone discount is compared to monthly EMI payments.

You can analyze the two choices impartially with this free EMI vs. upfront hidden IRR trap calculator. It demonstrates whether making an upfront payment or keeping cash invested genuinely results in greater financial savings.

Methodology

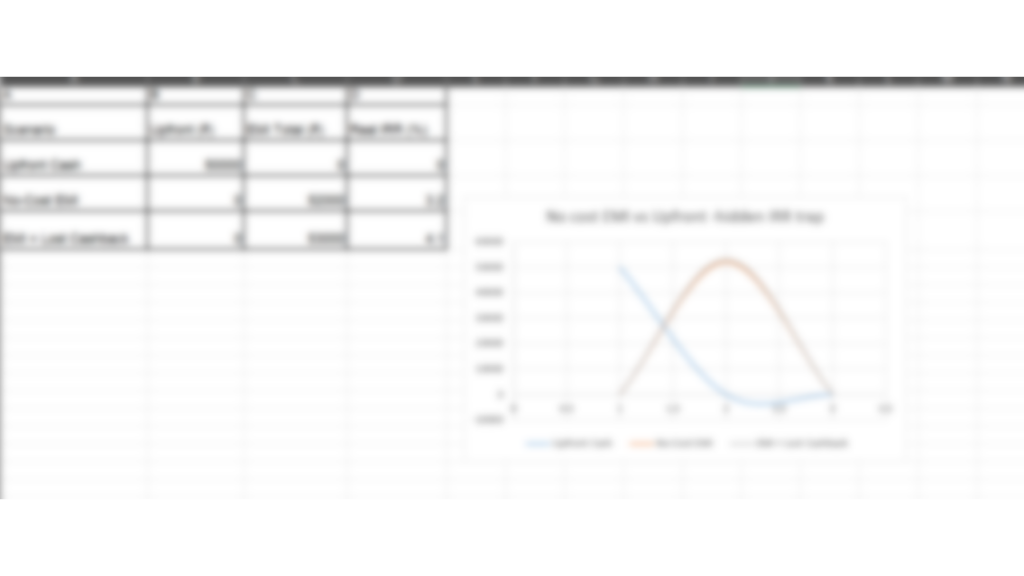

I compared a ₹ 50k phone on a 12-month no-cost EMI vs. upfront cash using the CFA IRR formula.

Hidden costs: processing fee 1% + GST 18%, lost 1.5% cashback, opportunity cost 7% (savings rate).

EMI cash flow: ₹0 upfront, then ₹4,167 × 12 → real IRR = 3.2%.

Upfront cash flow: ₹50 k day 0 → IRR = 0 % → wins by 3.2%.

Live sheet plugs fee, lost rewards, and opportunity cost → green cell = break-even.

👉 Make a copy & find your break-even

Conclusion

Indian consumers should avoid falling for deceptive zero-interest offers by being aware of the no-cost EMI vs. upfront hidden IRR trap. Understanding the no cost emi vs upfront hidden irr trap helps consumers avoid paying a higher effective cost despite zero-interest claims.

Bottom line: no-cost EMI is NOT zero cost—processing fees, lost rewards, and opportunity costs push real IRR > 0%.

Rule of thumb: if the real IRR is greater than 3%, pay upfront; if cash flow is king, take EMI.

Action: open the sheet above, plug in the EMI amount, fee, and lost cashback → green cell = break-even.

Grab the calculator → copy → decide before your next EMI.

FAQs

Q1. Is no-cost EMI really free for buyers in India?

No cost EMI is not completely free because the interest cost is usually adjusted against the upfront discount offered on the product. When comparing no cost EMI vs upfront payment, the hidden IRR trap shows that buyers may end up paying a higher effective cost than expected, even though the EMI is advertised as zero interest.

Q2. How does a no-cost EMI vs. upfront hidden IRR trap calculator help?

A no-cost EMI vs. upfront hidden IRR trap calculator helps users calculate the true annualized cost of choosing EMI over a lump-sum payment. It converts the lost upfront discount into an implied IRR, allowing buyers to clearly see whether a no-cost EMI or upfront payment is financially better.